Stressed global water resources and escalating demands on those resources are creating unprecedented risks that threaten economic activity and human well-being. Population growth and mounting climate change impacts are compounding these threats.

Industry—from food production to mining, apparel manufacturing to high-tech—collectively is the single largest user and influencer of water resources globally. It has much to lose from the critical risks arising from water scarcity, pollution, and broader hydrological disruptions. It is also uniquely positioned to mitigate these challenges through adopting a range of better water management practices.

Food and agricultural production accounts for 70% of water withdrawals globally, while other industries such as energy, mining, and manufacturing account for another 19%. Given this, it will be impossible to significantly advance global water security without stronger private sector leadership, both from companies and the institutional investors that own them [1]. The risks of inaction are extremely high—not just for the long-term sustainability of businesses, industries, and entire economies—but critically for the millions of people globally whose health and livelihoods are threatened by irresponsible water management.

All industries need water to operate, and many companies have taken important steps in recent years, oftentimes voluntarily, to improve their water stewardship – an encouraging indicator of the enormous potential for scaling up water management best practices [2]. Still, the overall responses to date have been broadly insufficient.

This report is a first-of-its-kind comprehensive scientific review and analysis of the perilous global water landscape – focusing specifically on how key industry practices are critically affecting global freshwater resources. Through an extensive literature review, the report also identifies the multiple chronic and systemic risks to surface and groundwater resources. It also explores what the private sector (both companies and the investors that own them) can do to strengthen water stewardship globally.

Global hot spots for changing freshwater availability

Figure 1. Data collected from NASA’s Gravity Recovery and Climate Change (GRACE) satellites shows places where freshwater resources are rapidly increasing (e.g. due to increasing flooding) in deep blue. Places where freshwater resources are rapidly decreasing (e.g. due to prolonged drought, groundwater depletion, or melting ice) are shown in deeper reds. These rapid changes are largely human driven and result from climate change and unsustainable water exploitation [3].

How Industry Affects Freshwater Resources

Decades of scientific and empirical evidence make clear that wide-ranging industrial activities, especially from agricultural supply chains and industries within the consumer staples sector, are putting considerable pressure on freshwater systems through changes in water availability, water quality, and ecosystem alterations, such as wetland destruction, river diversions, and irrigation (Figure 1). This evidence underscores that industry is a critical part of the global hydrologic system, along with natural processes and direct human use.

Water availability

Food products and other industries are threatening water availability globally, especially groundwater resources that are being drained faster than their natural recharge capacity. A 2019 study estimates that by 2050, 42% to 79% of watersheds that pump groundwater globally could surpass ecological tipping points without better water management [4]. Many of the worst hot spots are in heavily populated countries, such as India, which relies almost entirely on groundwater for food production. While crop-related irrigation is the biggest driver of water scarcity, resource extraction activities, such as mining and oil and gas production (especially hydraulic fracturing) can also cause severe localized water scarcity, particularly in regions with high water stress. The apparel industry, largely due to cotton production, has also triggered catastrophic localized water shortages.

Water pollution

Water contamination, whether from metals, plastics, pharmaceuticals, synthetic fertilizers, or manure, is another escalating threat that is being caused almost entirely by industrial activities and consumer waste. By nearly every measure, water pollution levels are rising in developed and developing countries alike.

Agriculture (fertilizers, manure, sediment, pesticides, and pharmaceuticals) and household products (soaps and detergents) are primary contributors to excessive nonpoint pollution into streams, rivers, and estuaries, resulting in toxicity and low-oxygen eutrophic ‘dead’ zones that are spreading worldwide. Metal pollution, mostly from metals, mining, and technology manufacturing, is another growing threat, especially in developing countries lacking environmental regulations and adequate wastewater treatment.

Plastic waste, especially microplastics, is another growing problem that is traceable to multiple industrial sectors, with the biggest footprint being in Asia. Poor waste management is a significant factor in plastic pollution. Much of this plastic ends up in surface waters and oceans, entangling and poisoning species and bioaccumulating in the human food chain. Pharmaceuticals and a group of artificial chemicals known as perfluoroalkyl and polyfluoroalkyl substances (PFAS) are additional evolving threats.

Water diversions/Ecosystem alterations

Industry’s contribution to natural ecosystem destruction is also a critical factor in water stress and biodiversity loss, whether from the filling of wetlands for site operations or agricultural fields to the razing of forests for cattle raising. Water engineering and infrastructure projects designed to make freshwater available for industrial uses, such as agriculture, energy production, and other economic activities, are altering natural water flows and critical habitats globally. The dam-building frenzy that marked the 20th century in the U.S. is now happening on a far larger scale globally [5]. In addition to high evaporative losses, dam projects can also cause increased salinization, nutrient enrichment, and reduced sediment loads. They can also cause major negative socioeconomic impacts, including relocation of communities and increased probability of user conflicts.

How Freshwater Resources Affect Industry

The relationship between industries and freshwater systems should be broadly viewed as a two-way interaction, meaning that freshwater resources affect industry just as industry affects freshwater. It is important to realize that declining water availability and water degradation, as well as climate change impacts, such as increased flooding and drought, are profound financial risks that industries must recognize and respond to more affirmatively.

A recent Barclays’ research note warned that the consumer staple sector alone, including agriculture, food, and beverage companies, is facing a potential $200 billion impact from water scarcity risks – roughly three times higher than carbon-related risks[6]. A 2020 CDP report, based on data from nearly 3,000 companies, warned of even larger business losses, potentially eclipsing $300 billion if water risks were not mitigated [7].

Water scarcity

Water conflicts between companies and local communities are becoming more commonplace in places like India and the U.S. and will likely worsen as populations swell and water becomes scarcer. Beverage companies have been in the spotlight due to such conflicts. In some instances, bottled water brands were forced to close groundwater wells due to water scarcity and pollution concerns from the community. Food and agriculture companies also face water availability risks. Declining water tables are already causing devastating financial impacts for farmers in India, including higher pumping costs and reduced crop yields. Droughts and groundwater depletion in California have forced farmers to leave millions of acres unplanted in recent years. The mining and energy sectors are also vulnerable to localized water shortages, whether from depleted groundwater aquifers that stop a mining project in its tracks or drought conditions that can throttle hydroelectric production.

Supply chain disruptions

Global supply chains for numerous industries are increasingly vulnerable to water-related risks, many of them tied to climate-driven extreme weather events, such as flooding and drought. The total cost of damages (direct physical damages across numerous industries and residential properties, as well as public infrastructure) from water disasters (droughts and floods) in the U.S. is estimated to be nearly $1 trillion since 1980 [8]. In just the first eight months of 2021, extreme flooding in central China shut down coal deliveries, which led to widespread power shortages; flooding and landslides in western Europe disrupted rail traffic for steelmakers and other producers that were unable to get raw materials; the worst drought in half a century in Taiwan in the summer of 2021 deepened the shortage in semiconductors, which use large amounts of water to produce [8]. In the last quarter of 2021, a once-in-a-century flood in British Columbia disrupted supply chains both in Canada and the U.S. for months. Industries that have limited supply chains geographically can be especially vulnerable to these kinds of disruptions. Heavy rare earth metals, which are critical to aerospace, electric vehicle, medical appliances, and other electronic sectors, are geographically concentrated in southeastern China, which is especially prone to climate hazards, including extreme rainfall events. It is estimated that each extreme rainfall event or a series of such events causes at least a 20% decrease in heavy rare earth production in this region due to flooding, mine site damages and disrupted logistics [9].

Climate change – a threat multiplier

Human-caused climate change is disrupting global water cycles that drive precipitation and weather patterns in every corner of the planet – disruptions that are already cascading across major industries and their supply chains. The November 2021 report from the International Panel on Climate Change (IPCC) found that “global warming is projected to further intensify the global water cycle,” from more extreme floods and droughts to changing rainfall patterns [10]. Warming global temperatures are already causing detectable changes that are throwing our delicate global climate system off balance. Melting polar ice caps are causing rising sea levels, threatening major population centers and critical agriculture zones. Melting glaciers and continental ice sheets are also changing streamflow patterns in the headwaters of the world’s rivers and are jeopardizing aquatic ecosystems and freshwater supplies for one sixth of the world’s population.

Added together, these cumulative risks are already having profound financial and social consequences, known as economic externalities, that are not reflected in day-to-day business costs. This is largely the result of global economic systems continuing to treat water as an infinite resource with little value, leading to widespread waste and misuse. The ‘true cost’ of water is estimated to be at least three times higher than what companies currently pay, once direct and indirect costs of water shortages and other risks are incorporated[11]. The urgency for industries, institutional investors, and policymakers to address this misalignment – so that water is treated as a finite and precious resource – should be crystal clear.

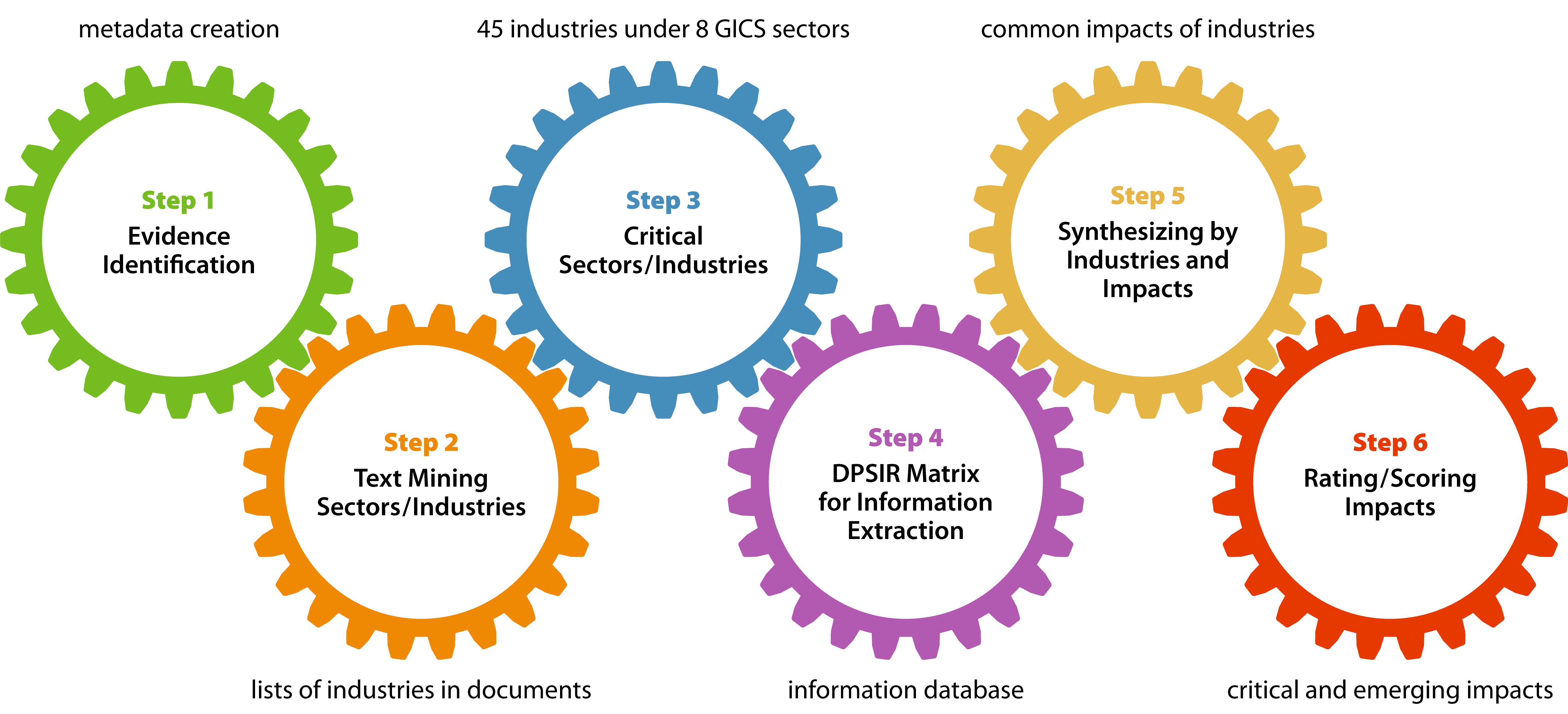

Scope, Goals, and Methodology

Figure 2. Overall approach to industrial water impacts identification

As summarized in Figure 2, this assessment reviews and synthesizes the scientific literature to identify the critical sectors and industries impacting freshwater and the industry practices leading to water impacts. Through the scientific evidence and literature review, the report also includes how these damaging impacts pose long-term financial risks, especially as population growth and climate change impacts ripple across the world.

The Driver-Pressure-State-Impact-Response (DPSIR) [12] model was applied as a conceptual framework to guide information extraction from research papers. The model was then again used to synthesize evidence that describes the causal chain of how various industrial practices and activities affect freshwater systems and societal responses to these impacts, such as regulations, measurement, and laws. Based on the causal chain, critical impacts and associated practices were identified according to the intensity and severity that have been reported in the literature. The DPSIR framework was developed by the European Environment Agency as an extension of the previous Pressure-State-Response model from the Organization for Economic Co-operation and Development (OECD). The assessment used a four-tiered industrial classification system, known as the Global Industry Classification Standard (GICS), to classify companies based on their principal business activities. Finally, using a comprehensive systematic literature review process, the assessment identified critical sectors and industries and their impacts (Appendix B).

Using this methodology, the following key GICS sectors (and associated industries) causing significant impacts to freshwater resources are identified: Consumer Staples (food, beverage, household and personal products), Consumer Discretionary (apparel, textiles, automobiles, household durables, and hotel, restaurants, and leisure), Energy (oil and gas and consumable fuels), Industrials (building/ construction, electroplating, and marine), Health Care (pharmaceuticals, health care services, and providers), Information Technology (high-tech and electronic, semiconductor and circuit board, and battery), Materials (metal and mining, chemicals, paper and forest products, and construction materials), and Utilities (renewable electricity and electric utilities).

It should be noted that the industries included in this report were widely reported upon in the academic literature as having significant impacts on freshwater resources. This does not imply that those industries not mentioned in this report have less or no adverse impacts on water. Rather, it means that they were not well represented in academic literature. Many of these missing industries are also contributing to escalating water risks. The cumulative impacts of industry on water require comprehensive action by all sectors to address one of the biggest risks mankind has ever faced—the water crisis.

The Role of Investors - Understanding Water Risk as Financial Risk

Currently, many of the world’s largest institutional investors have not integrated the widespread impacts of private sector activities on freshwater into their investment and engagement practices. There is a limited awareness of the degree to which certain corporate practices are both severe and systemic in nature, threatening the freshwater resources that economies and societies depend on and creating far-reaching financial risks for companies and investors themselves.

This analysis brings together scientific and financial research in a way that summarizes for the investor community the extent of these impacts and sectors and associated industries that are causing the most harm and have the most to lose if improvements are not made. Financial institutions can then apply this scientific evidence to their own investment process to understand how their investments are impacting water resources, how broadly they are exposed to water-related risks, and how they can engage with companies and industries that they invest in to halt the widespread systemic harm these sectors are causing. For instance, this research was recently used to inform two materiality briefs, published by Ceres in partnership with Bluerisk, DWS, and S&P Sustainable1, focused on the cost of action to address water impacts created by two high impacting industries, apparel and packaged meat (food products)[13],[14]. The analysis found that the impacts are so harmful they could cost up to $1.8 billion annually for some of the firms to address--though the cost of inaction could be five times higher [7].

Capital market players have a critical role to play in addressing the global water crisis. This report is part of the work of the Valuing Water Finance Initiative, a partnership between Ceres and the Government of the Netherlands and other stakeholders, to advance large-scale change in corporate water practices and water-related financial risks. To ensure the analysis is relevant to a capital markets audience, the Valuing Water Task Force, made up of major institutional investors and banks, provided input as part of the review process that included a scientific advisory committee, the Valuing Water Stakeholder Working Group, and other experts.